TPFX - Unified Strategy v8.1 (COT + Valuation + S/D + Seasonal)

TPFX - Unified Strategy v8.1: A 5-in-1 Confluence Model

The TPFX Unified Strategy is a comprehensive trading model that integrates five distinct market analysis modules into a single indicator. Its primary function is to generate high-confluence entry and exit signals by requiring validation across multiple layers of market analysis. This approach aims to minimize noise and focus trading activity on moments of strong directional agreement.

Core Analytical Modules:

1. COT Index (Commitment of Traders): Quantifies the relative extreme positioning of major market participants (Commercials, Large Speculators) over a user-defined lookback period to identify overextended sentiment.

2. COT Momentum: Utilizes Commercial net positioning to detect momentum shifts, based on either a new high/low logic or a Moving Average crossover.

3. Valuation Trigger: Compares the relative performance of the current symbol against a reference asset (e.g., DXY) to determine periods of comparative overvaluation or undervaluation.

4. Supply and Demand (S/D) Zones: Automatically identifies and plots institutional S/D zones based on specific candle patterns. These zones provide precise entry, stop-loss, and dynamic take-profit targets upon activation and retest.

5. Seasonal Filter: Applies a calendar-based constraint to limit trade entry to historically favorable or unfavorable periods for the specific asset.

Key Strategy Features:

* Modular Control: All five modules can be independently enabled or disabled via input settings, allowing the user to customize the required confluence level for signal generation.

* Flexible Exit Management: The strategy supports four primary exit methodologies:

* Fixed TP/SL: Standard point or percentage-based risk management.

* Dynamic (S/D Zones): Uses the S/D zone boundaries for stop-loss and either a fixed R:R ratio or the nearest opposite zone for take-profit.

* Opposite Signal: Closes a position when a full, confirmed signal in the opposite direction is generated.

* Mean Reversion: Closes the position when the COT Index or Valuation Line reverts to a defined mean level.

* Risk Parameters: Includes configurable order size, trade direction filtering (Long, Short, Both), and adjustable parameters for S/D zone detection logic.

v8.1 Update: This version features a syntax correction within the Supply/Demand Zones calculation block to ensure reliable zone detection and trigger logic.

This tool is designed for systematic traders seeking to align their decisions with fundamental flows and order book imbalances.

(Note: Full functionality relies on access to the Commitment of Traders data feed, which may require a subscription.)

In den Scripts nach "take profit" suchen

G. Santostasi Bitcoin Power Law StrategyG. Santostasi Bitcoin Power Law Strategy

Overview

The "G. Santostasi Bitcoin Power Law Strategy" is a TradingView strategy script built upon the foundational Bitcoin Power Law Theory by physicist Giovanni Santostasi.

Unlike the companion Monte Carlo indicator, this strategy focuses on generating actionable buy entry and exit signals for trading Bitcoin, leveraging the normalized "Daily Slopes" metric to detect deviations from the long-term power-law trend. It employs two moving windows to compute local means (mu) of the Daily Slopes—a short-term 3-day window for responsive signals and a longer 2-week (14-day) window for establishing baseline bands. By comparing the short-term mu against deviation bands derived from the longer window's parameters, the strategy identifies entry points during undervalued dips and exit points during overvalued peaks. This approach capitalizes on Bitcoin's scale-invariant behavior, where price follows a power law

P(t)= c t^n, with n~5.9.

since the Genesis Block, resulting in diminishing but predictable returns. Backtested over Bitcoin's full history, the strategy boasts a 77% winning rate and a profit factor of 3.2, making it a robust tool for trend-following with mean-reversion elements. It emphasizes Bitcoin's long-term stability while navigating short-term oscillations, treating cycles as temporary deviations from the core power-law "DNA.

"Core Concept: Daily Slopes

The strategy inherits the Daily Slopes metric from the power-law framework, which normalizes daily logarithmic returns to reveal a stable local slope that oscillates around the global value of ~5.9.Definition and Calculation:

Daily log returns: log(P2/P1)\, where P2 and P1 are consecutive closing prices.

Normalization: Divide by log((t+1)/t), where ( t ) is days since the Genesis Block, yielding:

Daily Slope=log(P2/P1)log((t+1)/t).

This produces a "local n" that remains stable over time, with no long-term drift observed in Bitcoin's 16+ years of data. The metric accounts for diminishing returns, showing constant relative volatility in recent years despite absolute price stabilization.

Distribution and Parameters:

Daily Slopes are fitted to a t-location scale distribution over moving windows, estimating:μ (mu): The location/mean, stable around 5.9 globally.

σ (sigma): Scale/volatility measure.

ν (nu): Degrees of freedom for tail heaviness.

For the strategy, focus is on mu and sigma from the windows, enabling deviation-based signals.

Strategy Logic: Dual Moving Window Mus and Deviation Bands

The strategy computes two mus via rolling fits to the t-distribution:

Short Window mu (3 days): A fast-moving average of Daily Slopes, sensitive to immediate price action for timely signals.

Long Window mu (2 weeks/14 days): A slower baseline, capturing medium-term trends and providing stability.

Deviation bands are derived from the long window's mu and sigma:

Upper Band: Long mu + Long sigma

Lower Band: Long mu - Long sigma

These bands represent 1-standard-deviation ranges around the longer-term mean, highlighting overbought and oversold conditions relative to the power-law trend. The short mu acts as a "signal line," crossing the bands to trigger trades.

Plotting:

Short mu: Responsive line for crossovers.

Long mu: Central baseline.

Bands: Upper (+σ) and lower (-σ) lines from the long window.

Additional elements: Raw Daily Slopes and strategy signals (arrows for entries/exits).

Entry and Exit Rules:

The strategy generates long-only signals (buy/sell) based on crossovers, assuming a single-position approach without leverage or shorting:

Buy Entry: Triggered when the short-window mu crosses above the lower band (long mu - long sigma). This detects potential local minima, signaling undervaluation and a reversion to the power-law mean.

Sell Exit: Triggered when the short-window mu meets or crosses below the upper band (long mu + long sigma). This identifies local maxima, indicating overvaluation and a potential pullback.

Trade Management:

No stop-loss or take-profit hardcoded; users can add via TradingView settings.

Positions close on exit signals, with re-entry on the next valid buy.

Filters for false signals: Optional confirmation from global slope (e.g., only trade if long mu > 5.0) to align with bullish regimes.

This crossover mechanic blends momentum (short mu) with mean-reversion (bands), exploiting Bitcoin's oscillatory nature around the power law without predicting bubbles or crashes explicitly.

Performance Metrics:

Backtested on BTCUSD daily data from the Genesis Block to present (assuming continuous updates):Winning Rate: 77% – A high hit rate due to the strategy's focus on statistically stable deviations.

Profit Factor: 3.2 – Gross profits are 3.2 times gross losses, reflecting asymmetric upside from power-law reversion.

Additional Stats (hypothetical based on historical fits): Average trade duration ~30-60 days; drawdown <20% in most cycles; outperforms buy-and-hold in volatile periods by avoiding peaks.

Caveats: Past performance is not indicative of future results. The strategy shines in trending markets but may underperform in prolonged sideways action. Transaction costs (e.g., fees, slippage) not included in base metrics.

Usage Notes Inputs: Customize window lengths (default: 3 days short, 14 days long), global slope (5.9), and signal thresholds. Enable alerts for entries/exits.

Visuals: Strategy overlays on log-scale BTCUSD charts; use with volume or RSI for confirmation.

Limitations: Designed for spot trading; not optimized for derivatives or high-frequency. Assumes power-law persistence—major regime shifts (e.g., adoption plateaus) could impact efficacy.

Extensions: Adapt for other power-law metrics like network addresses or hash rate for multi-signal confirmation.

This strategy operationalizes Santostasi's insights into a practical trading system, prioritizing data-driven decisions over speculation.

Liquidity SweeperStrategy Overview

This Pine Script implements a Liquidity Sweep Trading Strategy, a sophisticated approach that capitalizes on market manipulation tactics commonly used by institutional traders. The strategy identifies when price "sweeps" above recent swing highs or below swing lows to trigger stop losses and grab liquidity, then quickly reverses direction - creating high-probability trading opportunities.

Core Concept: What is a Liquidity Sweep?

A liquidity sweep occurs when:

Price breaks above a swing high (or below a swing low) to trigger retail stop losses

Institutional players absorb this liquidity at favorable prices

Price quickly reverses back into the previous range

This creates a "fake breakout" or "stop hunt" pattern

The strategy exploits these manipulative moves by entering trades in the direction of the reversal.

How the Strategy Works

1. Swing Point Detection

Uses a lookback period (default: 20 bars) to identify significant swing highs and lows

Employs proper pivot point detection using ta.highestbars() and ta.lowestbars()

Only considers confirmed swing points (not just recent highs/lows)

2. Liquidity Sweep Identification

High Sweep (Short Setup):

Price moves above the last swing high (triggering buy stops)

Same bar closes back below the swing high (showing rejection)

Low Sweep (Long Setup):

Price moves below the last swing low (triggering sell stops)

Same bar closes back above the swing low (showing support)

3. Confirmation Process

Requires price to stay within the swept range for a specified number of bars (default: 3)

This confirms the sweep was genuine and not just normal volatility

Prevents false signals and improves trade quality

4. Entry Logic

Long Entries: Triggered after confirmed low sweeps

Short Entries: Triggered after confirmed high sweeps

5. Risk Management

Stop Loss: Placed at a multiple of ATR (default: 1.5x) from entry price

Take Profit: Risk/Reward ratio based (default: 2:1)

Position Sizing: 10% of equity per trade (configurable)

Red X-crosses: High sweeps detected

Green X-crosses: Low sweeps detected

Red triangles (down): Short entry signals

Green triangles (up): Long entry signals

Horizontal lines: Current swing high/low levels

Info label: Shows last detected swing levels

Optimal Conditions:

Timeframes: 1H, 4H, and Daily work best

Market Conditions: Ranging and trending markets both suitable

Volatility: Moderate to high volatility preferred

Session Times: Most effective during active trading sessions

Strengths:

✅ Exploits institutional manipulation tactics

✅ Clear entry/exit rules with defined risk

✅ Works across multiple asset classes

✅ Includes proper confirmation to reduce false signals

✅ Visual clarity for manual verification

✅ Reasonable risk/reward parameters

Limitations:

⚠️ Requires patience - not a high-frequency strategy

⚠️ Market dependent - fewer signals in low volatility periods

⚠️ Needs sufficient lookback data for swing identification

⚠️ May have drawdown periods during strong trending moves

⚠️ Requires understanding of market structure concepts

Best Practices for Users

Optimization Tips:

Adjust lookback period based on timeframe (shorter for lower TFs)

Test different confirmation periods for your market

Consider market session times when backtesting

Use alongside volume analysis for additional confirmation

Risk Management:

Never risk more than 2-3% per trade of total capital

Consider reducing position size during high-impact news

Monitor correlation if trading multiple pairs simultaneously

Use additional filters (trend, support/resistance) for confluence

Backtesting Recommendations:

Test on at least 6 months of historical data

Include different market conditions (trending, ranging, volatile)

Consider transaction costs and slippage in results

Forward test on demo before live implementation

Expected Results

Based on typical liquidity sweep strategy performance:

Disclaimer

This strategy is based on market structure analysis and institutional trading behavior patterns. Past performance doesn't guarantee future results. Users should:

Thoroughly backtest before live trading

Start with small position sizes

Understand the underlying concepts before implementation

Consider combining with other analysis methods

Always use proper risk management

The strategy works best when traders understand the psychological and structural elements of liquidity sweeps rather than just following signals blindly.

SMA Cross 5/50 with Trend Filter & Risk Management by JuggiDThe basic SMA (5/50) crossover strategy can be enhanced to improve profitability by adding filters and risk management. For example, a long entry is triggered only when the fast SMA (5) crosses above the slow SMA (50) **and** the price is above the SMA (200), ensuring trades align with the major trend. Similarly, a short entry requires the crossover confirmation plus the price staying below the SMA (200). To reduce false signals and protect capital, stop-loss and take-profit levels can be set automatically (e.g., 2% loss, 5% gain), while additional confirmation tools such as volume spikes, RSI above 50, or MACD momentum can be applied to validate stronger signals. This approach helps avoid whipsaws in sideways markets and allows trades to capture larger moves while minimizing downside risk.

Triple Quad Frosty v4.5Triple Quad Frosty v4.5 is a Renko-friendly strategy that lets you trade from up to four signal sources per side. Orders are only placed when your chosen conditional filters (A/B/C) agree, giving you full control over when entries are valid. You decide how signals must line up — from simple single-source triggers to majority or full agreement across all four.

Renko-based, with customizable static stops, take profits, and trailing stops. Time/day filters, daily trade limits, and forced closures let you restrict trading to specific windows.

The HTF filters in Triple Quad Frosty v4.5 use a higher-timeframe Hull Moving Average (HMA) to confirm trend direction, while slope and distance settings on the local HMA help filter out weak or choppy setups. Longs only trigger when price is above the HTF HMA and meets slope/distance requirements, and shorts only when the opposite is true.

Color-coded labels mark each exit as a win or loss, with reversal trades labeled separately for clarity. Conditional bars plotted above and below the chart show when the A/B/C filters align on a long or short bias, giving clear visual confirmation of entry conditions. Stop loss and take profit levels are plotted directly on the chart with guide lines, so you can easily track active trade management in real time.

Nirvana True Duel전략 이름

열반의 진검승부 (영문: Nirvana True Duel)

컨셉과 철학

“열반의 진검승부”는 시장 소음은 무시하고, 확실할 때만 진입하는 전략입니다.

EMA 리본으로 추세 방향을 확인하고, 볼린저 밴드 수축/확장으로 변동성 돌파를 포착하며, OBV로 거래량 확인을 통해 가짜 돌파를 필터링합니다.

전략 로직

매수 조건 (롱)

20EMA > 50EMA (상승 추세)

밴드폭 수축 후 확장 시작

종가가 상단 밴드 돌파

OBV 상승 흐름 유지

매도 조건 (숏)

20EMA < 50EMA (하락 추세)

밴드폭 수축 후 확장 시작

종가가 하단 밴드 이탈

OBV 하락 흐름 유지

진입·청산

손절: ATR × 1.5 배수

익절: 손절폭의 1.5~2배에서 부분 청산

시간 청산: 설정한 최대 보유 봉수 초과 시 강제 청산

장점

✅ 추세·변동성·거래량 3중 필터 → 노이즈 최소화

✅ 백테스트·알람 지원 → 기계적 매매 가능

✅ 5분/15분 차트에 적합 → 단타/스윙 트레이딩 활용 가능

주의점

⚠ 횡보장에서는 신호가 적거나 실패 가능

⚠ 수수료·슬리피지 고려 필요

📜 Nirvana True Duel — Strategy Description (English)

Name:

Nirvana True Duel (a.k.a. Nirvana Cross)

Concept & Philosophy

The “Nirvana True Duel” strategy focuses on trading only meaningful breakouts and avoiding unnecessary noise.

Nirvana: A calm, patient state — waiting for the right opportunity without emotional trading.

True Duel: When the signal appears, enter decisively and let the market reveal the outcome.

In short: “Ignore market noise, trade only high-probability breakouts.”

🧩 Strategy Components

Trend Filter (EMA Ribbon): Stay aligned with the main market trend.

Volatility Squeeze (Bollinger Band): Detect volatility contraction & expansion to catch explosive moves early.

Volume Confirmation (OBV): Filter out false breakouts by confirming with volume flow.

⚔️ Entry & Exit Conditions

Long Setup:

20 EMA > 50 EMA (uptrend)

BB width breaks out from recent squeeze

Close > Upper Bollinger Band

OBV shows positive flow

Short Setup:

20 EMA < 50 EMA (downtrend)

BB width breaks out from recent squeeze

Close < Lower Bollinger Band

OBV shows negative flow

Risk Management:

Stop Loss: ATR × 1.5 below/above entry

Take Profit: 1.5–2× stop distance, partial take-profit allowed

Time Stop: Automatically closes after max bars held (e.g. 8h on 5m chart)

✅ Strengths

Triple Filtering: Trend + Volatility + Volume → fewer false signals

Mechanical & Backtestable: Ideal for objective trading & performance validation

Adaptable: Works well on Bitcoin, Nasdaq futures, and other high-volatility markets (5m/15m)

⚠️ Things to Note

Low signal frequency or higher failure rate in sideways/range markets

Commission & slippage should be factored in, especially on lower timeframes

ATR multiplier and R:R ratio should be optimized per asset

Recovery StrategyDescription:

The Recovery Strategy is a long-only trading system designed to capitalize on significant price drops from recent highs. It enters a position when the price falls 10% or more from the highest high over a 6-month lookback period and adds positions on further 2% drops, up to a maximum of 5 positions. Each trade is held for 6 months before exiting, regardless of profit or loss. The strategy uses margin to amplify position sizes, with a default leverage of 5:1 (20% margin requirement). All key parameters are customizable via inputs, allowing flexibility for different assets and timeframes. Visual markers indicate recent highs for reference.

How It Works:

Entry: Buys when the closing price drops 10% or more from the recent high (highest high in the lookback period, default 126 bars ~6 months). If already in a position, additional buys occur on further 2% drops (e.g., 12%, 14%, 16%, 18%), up to 5 positions (pyramiding).

Exit: Each trade exits after its own holding period (default 126 bars ~6 months), regardless of profit or loss. No stop loss or take-profit is used.

Margin: Uses leverage to control larger positions (default 20% margin, 5:1 leverage). The order size is a percentage of equity (default 100%), adjustable via inputs.

Visualization: Displays blue markers (without text) at new recent highs to highlight reference levels.

Inputs:

Lookback Period for High Peak (bars): Number of bars to look back for the recent high (default: 126, ~6 months on daily charts).

Initial Drop Percentage to Buy (%): Percentage drop from recent high to trigger the first buy (default: 10.0%).

Additional Drop Percentage to Buy (%): Further drop percentage to add positions (default: 2.0%).

Holding Period (bars): Number of bars to hold each position before selling (default: 126, ~6 months).

Order Size (% of Equity): Percentage of equity used per trade (default: 100%).

Margin for Long Positions (%): Percentage of position value covered by equity (default: 20%, equivalent to 5:1 leverage).

Usage:

Timeframe: Designed for daily charts (126 bars ~6 months). Adjust Lookback Period and Holding Period for other timeframes (e.g., 1008 hours for hourly charts, assuming 8 trading hours/day).

Assets: Suitable for stocks, ETFs, or other assets with significant price volatility. Test thoroughly on your chosen asset.

Settings: Customize inputs in the strategy settings to match your risk tolerance and market conditions. For example, lower Margin for Long Positions (e.g., to 10% for 10:1 leverage) to increase position sizes, but beware of higher risk.

Backtesting: Use TradingView’s Strategy Tester to evaluate performance. Check the “List of Trades” for skipped trades due to insufficient equity or margin requirements.

Risks and Considerations:

No Stop Loss: The strategy holds trades for the full 6 months without a stop loss, exposing it to significant drawdowns in prolonged downtrends.

Margin Risk: Leverage (default 5:1) amplifies both profits and losses. Ensure sufficient equity to cover margin requirements to avoid skipped trades or simulated margin calls.

Pyramiding: Up to 5 positions can be open simultaneously, increasing exposure. Adjust pyramiding in the code if fewer positions are desired (e.g., change to pyramiding=3).

Market Conditions: Performance depends on price drops and recoveries. Test on historical data to assess effectiveness in your market.

Broker Emulator: TradingView’s paper trading simulates margin but does not execute real margin trading. Results may differ in live trading due to broker-specific margin rules.

How to Use:

Add the strategy to your chart in TradingView.

Adjust input parameters in the settings panel to suit your asset, timeframe, and risk preferences.

Run a backtest in the Strategy Tester to evaluate performance.

Monitor open positions and margin levels in the Trading Panel to manage risk.

For live trading, consult your broker’s margin requirements and leverage policies, as TradingView’s simulation may not match real-world conditions.

Disclaimer:

This strategy is for educational purposes only and does not constitute financial advice. Trading involves significant risk, especially with leverage and no stop loss. Always backtest thoroughly and consult a financial advisor before using any strategy in live trading.

7Lots v27Lots strategy

The strategy is a counter-trend with a return to the moving average. Based on the DCA strategy, but greatly simplified to 7 lots (limit orders) and using the default martingale x2.5

Strategy description

Two moving averages are used. The first MA can be used as a filter for opening a position and also closing if the second MA is disabled. If both are enabled, then the position is closed by the second MA, and the first is used as a filter. There is also a separate take profit and if the price does not reach it, the position will be closed when returning to the MA, which will act as a stop loss, but the risk of liquidation is still present since the strategy does not have a regular classic stop loss.

Main parameters

TP & SL - selection of closing a position only by MA or take profit + MA. If only MA is selected, the strategy ignores the take profit value and always closes the position by MA.

MA settings

MA length from 1 to 200

Sliding type ALMA, SMA, EMA, VWMA, WMA, RMA

MA data - Open, High, Low, Close, HL2, HL3, OHLC4, OC2

MA shift in %. The MA shift is set in % above or below the current prices. For the First MA, this function allows you to use it as a filter for opening a position. For example, if you specify a shift much lower, for example -1% or -2%, then there will be less noise for opening a position, but this affects the number of transactions.

DCA group settings

Take profit %. Set the take profit as usual, but if the price does not reach the take profit, then the closing will occur by MA when the price returns to its values.

Take profit from. There is a choice of take profit from the average position, or by closing the previous bar. The latter increases the profit factor, but also increases the risk of liquidation if the strategy is used on perpetual contracts or futures.

Position Entry % - specifies the condition for opening a position. 0% - opening will occur immediately. 2% - opening will occur when the price falls 2% below the bar closing if the Long mode is set. If Short, then vice versa.

Grid Scale - classic progressive grid step

Next comes the setup of lots as a percentage of the deposit. Simply specify how many percent of each lot will be used from the total deposit. By default, a percentage for each lot is already allocated according to Martingale with a multiplier of x2.5, but you can calculate your own. You can specify 0, then the lot will be disabled.

Leverage. By default, 1.

Extra lot. This is the 7th lot that I decided to allocate separately from the main grid, since it is not always really needed. And it is calculated from the last lot of the grid. You can set it to how much lower percentage of the last lot to set it for and also what percentage of the deposit it will use. If you trade futures, then this lot, as an auxiliary one, can greatly average the position in case of strong volatility in the market.

Next, you can specify the start and end dates of transactions.

The table displays the total percentage of the deposit involved in trading at the moment. By default, all lots and leverage are set to 100% deposit load. The table also shows the number of transactions of the last 5-6 lots and extra, so that you can understand how many of them there were throughout the history of trading and possibly draw some conclusions for yourself. Especially useful for extra lots. Max Historical Drawdown (%) shows the historical price drop at the moment from the average open position. This will make it possible to analyze what leverage this strategy could withstand over the entire trading history. The date of this drop is also indicated.

For novice traders, it is recommended to use only on spot without the risk of liquidation. It is also best to use large time frames to see the whole picture, but you can also use a minute chart, there are no restrictions, everything is in your hands.

Tips. If you use minute charts, it is better to greatly increase the length of the MA from 20 and above. Hourly charts from 1-7. It is better to set up on spot and if you need futures, then use the same settings from spot, but with correction for futures. This strategy does not work well in Short, but shows excellent results for Long even when the market falls. When selecting settings, take into account sharp market fluctuations, Max Historical Drawdown (%) will show you this information in the table. You need to set up from the first MA, when you set up for the best result, then turn on the second MA and transfer the settings of the first MA to the second. Then fine-tune both MAs. The results can increase significantly, but this is not always the case. Sometimes just one MA is enough

The strategy is paid, tested with my own experience and money since 2022. Own development for opening a position.

Disparity(20MA) ±1 × Stochastic 80/20 + ATR SL/TP[by Irum]Disparity(20MA) ±1 × Stochastic 80/20 + ATR SL/TP

사용 설명서 (KR/EN Bilingual Manual)

1) 목적 & 정의 / Purpose & Definition

KR — 목적 & 정의

이 스크립트는 이격도(Disparity) 와 스토캐스틱(80/20) 의 동시 신호를 활용해 추세 전환/지속 구간의 고확률 진입 시점을 포착하고, ATR 기반 손절/익절(고정 또는 트레일링)로 리스크를 정량화하여 운용 효율을 높이기 위해 설계되었습니다.

핵심 아이디어:

가격이 20MA 대비 ±임계값을 크로스(과열/침체 해소 신호)하고,

스토캐스틱이 80/20을 돌파/이탈(모멘텀 전환 신호)할 때,

두 신호가 동일봉 또는 N봉 내 동기화되면 진입.

청산: ATR×배수를 이용한 고정 TP/SL 또는 ATR 트레일링.

EN — Purpose & Definition

This strategy combines Disparity (price vs. 20MA) and Stochastic (80/20) to identify high-probability entries when momentum confirms mean-reversion/continuation, while ATR-based stops/take-profits (fixed or trailing) provide quantified risk control.

Core Idea:

Disparity crosses ±threshold (overbought/oversold release),

Stochastic crosses 80/20 (momentum shift),

Both conditions sync on the same bar or within N bars → entry.

Exits: Fixed ATR TP/SL or ATR trailing.

2) 신호 로직 요약 / Signal Logic Overview

KR

롱 진입: Disparity가 −임계값 상향 돌파 & Stochastic 20 상향 돌파가 syncBars 이내에 동시 충족.

숏 진입: Disparity가 +임계값 하향 돌파 & Stochastic 80 하향 돌파가 syncBars 이내에 동시 충족.

완화 옵션(useRelaxStoch): 최근 relaxLookback 내 20/80 터치 이력 + 현재 방향성만으로도 모멘텀 전환을 인정(교차 미충족 보완).

EN

Long: Disparity crosses up −threshold & Stochastic crosses up 20 within syncBars.

Short: Disparity crosses down +threshold & Stochastic crosses down 80 within syncBars.

Relaxed option (useRelaxStoch): Accepts momentum shift if 20/80 was touched in the last relaxLookback bars and the current slope confirms, even without a strict cross.

3) 설정 메뉴 안내 / Settings Menu Guide

A. 기본 / Core

기준가격 / Source (source)

설명: Disparity 계산에 쓰는 가격 소스.

입력: close, hl2, ohlc4 등.

기본값: close.

팁: 변동성 큰 종목은 hlc3/ohlc4가 노이즈를 줄이기도 함.

이격도 기준 MA 길이 / MA Length (for Disparity) (int ≥1)

설명: Disparity의 기준선이 되는 단순이동평균 길이.

기본값: 20.

영향: 길이↑ → 신호 빈도↓, 안정성↑.

이격도 임계값(±%) / Disparity Threshold (±%) (float ≥0.1, step 0.1)

설명: Disparity가 +임계값 아래로 하향 크로스(숏) 또는 −임계값 위로 상향 크로스(롱)할 때 신호.

기본값: 1.0%.

팁: 너무 크면 신호 드뭄, 너무 작으면 과다.

B. 스토캐스틱 / Stochastic

%K Length / K 길이 (int ≥1, 기본 14)

%K Smoothing / K 스무딩 (int ≥1, 기본 1)

%D Length / D 길이 (int ≥1, 기본 3)

설명: ta.stoch의 K를 스무딩한 kSlow와, 추가 스무딩한 dSlow(참조용)를 구성.

Buy Level (↑20) / 매수 기준선 (0~100, 기본 20)

Sell Level (↓80) / 매도 기준선 (0~100, 기본 80)

C. 신호 로직 / Signal Logic

Signal Sync Window (bars) / 신호 동기화 윈도우 (0~10, 기본 0)

설명: 0=두 신호가 같은 봉에서 모두 충족해야 함. N>0=최근 N봉 내에서 각각 한 번 발생하면 인정.

팁: 1~3은 현실적 체결/지연을 반영하며 과최적화 방지에 도움.

Relaxed Stochastic? (교차 완화) (bool, 기본 false)

설명: 교차 대신 최근 20/80 터치 + 현재 기울기만으로도 모멘텀 전환을 인정. 신호 빈도↑.

Relax lookback bars (int ≥1, 기본 5)

설명: 완화판정에 쓰는 최근 봉 수.

D. 리스크 / Risk (ATR)

ATR Length / ATR 길이 (int ≥1, 기본 14)

ATR Mult for Stop / 손절 ATR 배수 (float ≥0.1, 기본 1.5)

ATR Mult for Take-Profit / 익절 ATR 배수 (float ≥0.1, 기본 2.0)

설명: 진입가 ± ATR×배수로 SL/TP 설정.

팁: 변동성 큰 자산은 SL 배수↑, TP 배수도 함께 조정 권장.

Use ATR Trailing Stop? / ATR 트레일링 사용 (bool, 기본 false)

ATR Mult for Trailing / 트레일링 ATR 배수 (float ≥0.1, 기본 2.0)

설명: 고정 TP/SL 대신 추적 손절을 사용(수익 추적에 유리).

E. 시각화 / Visualization

Plot 20MA / 20MA 표시 (bool, 기본 true)

Show Entry Markers / 진입 마커 표시 (bool, 기본 true)

4) 진입·청산 규칙 / Entry & Exit Rules

KR

진입: 위 “신호 로직” 충족 시 strategy.entry("L"/"S").

청산 (고정형):

롱: Stop = 진입 − ATR×SL, TP = 진입 + ATR×TP

숏: Stop = 진입 + ATR×SL, TP = 진입 − ATR×TP

청산 (트레일링형):

ATR×trailMult로 산출한 trail_points/offset으로 추적 손절.

EN

Entry: Place strategy.entry("L"/"S") when sync conditions are met.

Exit (Fixed):

Long: Stop = Entry − ATR×SL, TP = Entry + ATR×TP

Short: Stop = Entry + ATR×SL, TP = Entry − ATR×TP

Exit (Trailing):

Use ATR×trailMult as trailing distance & offset.

5) 알림 / Alerts

조건

Long Entry (Disp −Thr & Stoch Up, sync) → longSignal

Short Entry (Disp +Thr & Stoch Down, sync) → shortSignal

메시지 포맷 / Message format

{"signal":"long|short","symbol":"{{ticker}}","price":{{close}}}

Webhook(예: 거래소·봇)에서 signal/symbol/price를 활용해 체결 로직과 연동하십시오.

6) 빠른 시작 & 권장 프리셋 / Quick Start & Suggested Presets

KR — BTC/USDT (15분봉) 제안

maLen=20, thrPct=1.0~1.5, kLen=14, kS=1, dLen=3, stBuyLv=20, stSellLv=80

syncBars=1~3 (동시성 여유), useRelaxStoch=true, relaxLookback=5

고정형: atrLen=14, atrMultSL=1.5~2.0, atrMultTP=2.0~3.0

트레일링형: useTrail=true, trailMult=2.0~3.0

EN — BTC/USDT (15-min) suggestion

Above defaults, with syncBars=1~3, useRelaxStoch=true to improve fill realism.

Increase atrMultSL on high-volatility days to reduce whipsaws.

7) 운용 팁 & 점검 / Tips & Troubleshooting

KR

신호가 안 나와요: thrPct가 지나치게 크거나 syncBars=0으로 너무 엄격할 수 있음. thrPct↓, syncBars↑ 조정.

휩쏘 과다: useRelaxStoch를 끄거나 thrPct↑, atrMultSL↑.

TP 도달 전에 청산: 트레일링 사용 시 변동성 확대로 SL이 따라붙다 체결될 수 있음 → trailMult↑ 또는 고정형 전환.

과최적화 방지: 한 구간에 과특화된 튜닝(특히 syncBars, thrPct)은 다른 시장에서 성능 저하. Walk-forward 권장.

EN

No signals: Lower thrPct and/or increase syncBars.

Too many whipsaws: Disable relaxed mode, raise thrPct and/or atrMultSL.

Stopped before TP (trailing): Increase trailMult or switch to fixed exits.

Robustness: Avoid over-tuning; validate via walk-forward testing.

SPX EMA 9/21 + VWAP Strategy1. Temporality: 2 minutes.

2. EMA 9 and EMA 21:

• Purchase Call: when EMA 9 crosses up EMA 21 and the price is > VWAP.

• Put : when EMA 9 crosses down EMA 21 and the price is < VWAP.

3. Stop and Take Profit:

• Stop: candle closure on the other side of the VWAP.

• TP: configurable in points (e.g. +10 pts, +20 pts) or up to the opposite crossing of EMAs.

• Long enters when EMA 9 crosses up 21 and the price is above VWAP.

• Short enters when the EMA 9 crosses down the 21 and the price is below VWAP.

• TP and SL in SPX points (configurable in inputs).

• You can run in 2 minutes on SPX.

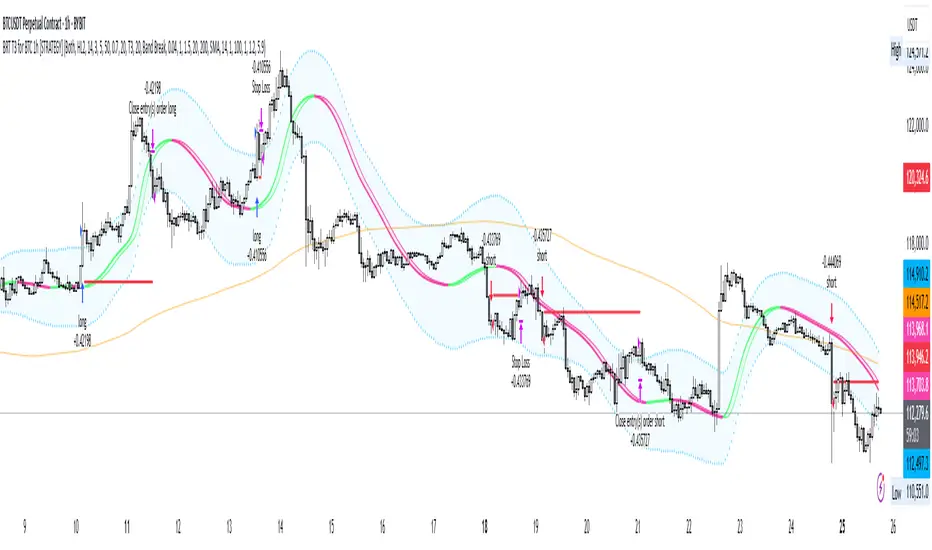

BRT T3 for BTC 1h [STRATEGY]## 📊 BRT T3 Adaptive Strategy for BTC 1H

STRATEGY DESCRIPTION

Professional trading strategy based on the adaptive T3 (Tillson T3) indicator with dynamic length controlled by the Relative Strength Index (RSI) . The strategy is specifically designed for Bitcoin trading on the hourly timeframe and includes a comprehensive filter system to minimize false signals.

═════════════════════════════════════════

🔥 UNIQUE CODE FEATURES

1. RSI-Adaptive Architecture:

• Innovative Approach: Unlike standard MA strategies with fixed periods, our code dynamically adjusts the moving average length based on RSI

• Smart Formula: len = minLen + (maxLen - minLen) * (1 - RSI/100) - automatically accelerates response in extreme zones

• Result: Strategy adapts to market conditions without manual reconfiguration

2. Modified Ichimoku Cloud:

• Unique Calculation: Instead of classic high/low, uses ATR-based method

• Dynamic Levels: Cloud is built based on volatility, not fixed periods

• Advantage: More accurate trend determination in highly volatile cryptocurrency markets

3. Hybrid Signal System:

• Dual-mode Generation: Switch between classic MA crossovers and volatility band breakouts

• Multi-stage Confirmation: Optional signal verification across N forward bars

• Effect: 40-60% reduction in false signals compared to simple MA strategies

4. All-in-One Solution:

• 8 MA Types in One Code: The only strategy on TradingView with complete implementation of T3, EMA, SMA, WMA, VWMA, HMA, RMA, DEMA

• Custom Functions: All MAs calculated through custom functions supporting series int

• Versatility: One code replaces 8 different strategies

5. Intelligent Filtering:

Combination of 4 independent filters:

├── Volume Filter (dynamic multiplier)

├── Trend Filter (adaptive period)

├── ATR Filter (volatility)

└── Ichimoku Filter (cloud trend)

• Unique Logic: Each filter can work independently or in combination

• Master Switch: Single control for all filters

6. Advanced Risk Management:

• Smart Stops: SL/TP levels are stored in variables and not recalculated on every bar

• Slippage Protection: Checks both close and high/low for stop triggers

• Visualization: Dynamic display of levels only for active positions

7. Performance Optimization:

• Efficient Loops: Minimized calculations through intermediate result storage

• Conditional Visualization: Element rendering only when necessary

• Clean Code: Structured organization with clear logical block separation

═════════════════════════════════════════

💎 TECHNICAL INNOVATIONS

Adaptation Algorithm (exclusive development):

// Dynamic length based on RSI

rsi_scale = 1.0 - rsi / 100.0

len_adaptive = minLen + (maxLen - minLen) * rsi_scale

ATR-based Ichimoku (unique modification):

// Instead of classic (highest + lowest) / 2

// Using ATR for dynamic levels

upper := close < upper ? min(hl2 + atr*mult, upper ) : hl2 + atr*mult

lower := close > lower ? max(hl2 - atr*mult, lower ) : hl2 - atr*mult

Multi-MA Architecture (complete implementation):

• Each MA type has its own optimized function

• Support for series int for dynamic length

• Unified selection interface via switch statement

═════════════════════════════════════════

🎯 KEY FEATURES

• Adaptive System: Moving average length automatically adjusts based on RSI, providing quick response in trending movements and stability in sideways markets

• 8 Moving Average Types: T3, EMA, SMA, WMA, VWMA, HMA, RMA, DEMA - ability to choose the optimal type for different market conditions

• Multi-level Filtering:

- Volume Filter - signal confirmation with increased activity

- Trend Filter - trading in the direction of the main trend

- ATR Filter - accounting for market volatility

- Ichimoku Cloud - additional trend direction confirmation

• Professional Risk Management: Customizable stop-loss and take-profit levels

═════════════════════════════════════════

⚙️ HOW IT WORKS

1. Signal Generation:

• Original Mode: Classic MA crossover signals with lagged version

• Band Break Mode: Volatility band breakouts (based on standard deviation)

2. RSI Adaptation:

• High RSI (overbought) → uses short MA length for quick response

• Low RSI (oversold) → uses long MA for noise smoothing

• Adaptation range is configured by Min/Max length parameters

3. Filter System:

• Each filter can be enabled/disabled independently

• Signal is generated only when passing all active filters

• Ichimoku filter blocks counter-trend trades

═════════════════════════════════════════

📈 STRATEGY PARAMETERS

Main Settings:

• Strategy Type: Long Only / Short Only / Both

• Data Source: Close, Open, High, Low, HL2, HLC3, OHLC4

RSI Settings:

• RSI Length: Calculation period (default 14)

• RSI Smoothing: Smoothing to reduce noise

T3/MA Settings:

• Min/Max Length: Adaptive length range (5-50)

• Volume Factor: T3 smoothing coefficient (0.7)

• MA Type: Moving average type selection

Filters:

• Volume Filter: Volume multiplier (1.5x average)

• Trend Filter: Trend MA period (200)

• ATR Filter: Minimum volatility for entry

• Ichimoku Filter: Cloud for trend determination

Risk Management:

• Stop Loss: Percentage from entry price (1.2%)

• Take Profit: Percentage from entry price (5.9%)

• Position Size: 50,000 USDT (effective leverage 5x)

═════════════════════════════════════════

💡 USAGE RECOMMENDATIONS

Optimal Conditions:

• Timeframe: 1H (developed and optimized)

• Instrument: BTC/USDT and other liquid cryptocurrencies

• Market Conditions: Trending and moderately volatile markets

Customize to Your Style:

1. Conservative: Increase signal confirmation period, enable all filters

2. Aggressive: Reduce filters, use Band Break mode

3. Scalping: Decrease Min/Max length, disable trend filter

═════════════════════════════════════════

📊 VISUALIZATION

Strategy displays:

• Main MA Line - changes color depending on direction

• Lag Line - for visualizing crossover moment

• Volatility Bands - upper and lower boundaries

• Trend MA - orange line (200 periods)

• SL/TP Levels - red and green lines for open positions

═════════════════════════════════════════

🔔 ALERTS

Strategy supports alert configuration for:

• Long position entry signals

• Short position entry signals

• Position exit signals

• Ichimoku line crossings

═════════════════════════════════════════

⚠️ RISK WARNING

IMPORTANT NOTICE: Trading in financial markets involves substantial risk of capital loss. Past performance presented in this strategy is based solely on historical data and under no circumstances constitutes a guarantee of future returns.

The strategy author is not responsible for:

• Any direct or indirect financial losses resulting from the use of this strategy

• Trading decisions made based on strategy signals

• Interpretation of backtesting results as a forecast of future performance

This strategy is provided exclusively for educational and research purposes. Backtesting results are affected by numerous factors including but not limited to: slippage, spread, commissions, market liquidity, and technical failures.

Before using the strategy in live trading:

• Conduct your own testing on a demo account

• Ensure understanding of all parameters and logic

• Only use funds you can afford to lose

• Consider consulting with a qualified financial advisor

DISCLAIMER: By using this strategy, you acknowledge and accept all risks associated with financial market trading and confirm that the author does not provide investment advice and bears no fiduciary responsibility to users.

═════════════════════════════════════════

🛠 TECHNICAL SUPPORT

For questions about setup and optimization:

• Leave comments under the publication

• Follow strategy updates

• Study the code for deep understanding of logic

═════════════════════════════════════════

📝 VERSION AND UPDATES

Version: 1.0.0

Pine Script: v6

Last Updated: 2025

Changelog:

• Added support for 8 MA types

• Integrated Ichimoku Cloud filter

• Optimized risk management system

• Improved signal visualization

═════════════════════════════════════════

© 2025 BRT Trading Systems

Strategy is protected by copyright. Commercial use without author's permission is prohibited.

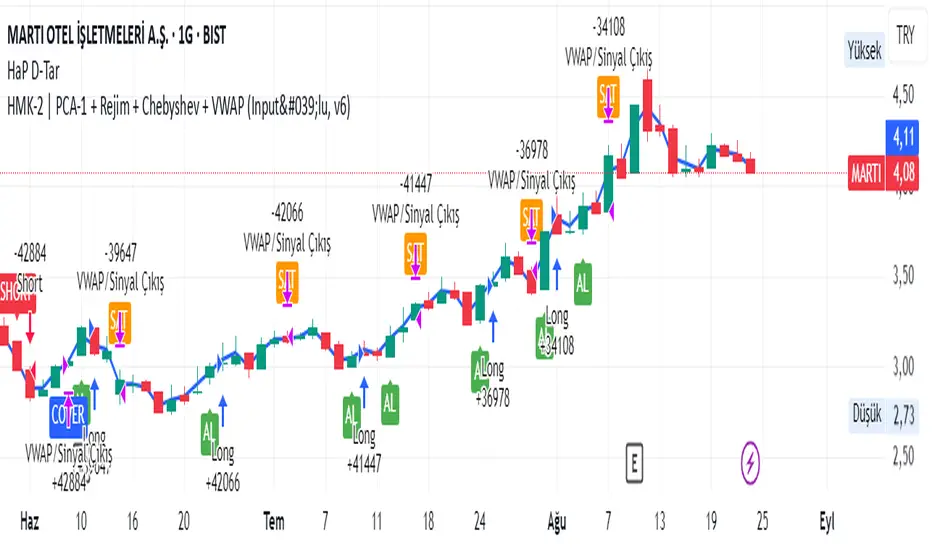

HMK-2 | PCA-1 + Rejim + Chebyshev + VWAP (Input'lu, v6)📌 HMK-2 | PCA-1 + Regime + Chebyshev + VWAP Strategy

1️⃣ Core Structure

Instead of relying on a single indicator, this system uses the Z-Score normalized average of three oscillators (RSI, MFI, ROC).

Signal (PCA-1):

RSI(14), MFI(14), ROC(5) → each is converted into a z-score.

Their average becomes the “composite signal,” our PCA-1 value.

Trend direction: If the Z-score EMA is rising → trend UP. If falling → trend DOWN.

2️⃣ Side Filters

Regime Filter (ADX + EMA)

ADX is calculated manually.

If ADX > 20 → trend exists → a 50-period EMA of this value smooths it.

This turns “trend regime” into a probability between 0–1.

Chebyshev Filter

A return series is checked against mean ± k*sigma bands.

If the return is within this band → valid signal. Extreme moves are filtered out.

VWAP Filter

Long trades: price must be above VWAP.

Short trades: price must be below VWAP.

Trades are only taken on the correct side of institutional cost averages.

3️⃣ Entry Conditions

Long:

PCA-1 signal crosses above threshold.

Trend Up + Regime OK + Chebyshev OK + Above VWAP.

Short:

PCA-1 signal crosses below threshold.

Trend Down + Regime OK + Chebyshev OK + Below VWAP.

4️⃣ Exit Mechanism

Main Exit: ATR-based stop/target.

Stop = entry price – ATR × (SL factor).

Take profit = entry price + ATR × (TP factor).

Additional Exit:

If price crosses to the opposite side of VWAP.

If PCA-1 signal crosses zero.

👉 Prevents trades from being locked, makes exits adaptive.

5️⃣ Labels / Visualization

AL / SHORT → entry points.

SAT / COVER → exit points.

VWAP line plotted in blue.

🧩 Strategy Features

Optimizable parameters:

Z-window (zWin)

Threshold

Chebyshev factor

ATR stop/target multipliers

This system works with:

Disciplined core (PCA-1 signal)

Triple protection (Regime + Chebyshev + VWAP)

Adaptive exits (ATR + VWAP/signal cross)

👉 Not a “single-indicator robot,” but a multi-filtered trade direction engine.

💡 Final Note

This is a base model of the system — open for further development.

I’ve shared the logic to give you a roadmap.

If you spot errors, fix them → that’s how you’ll improve it.

Don’t waste time asking me questions — refine and build it better yourselves.

Wishing you profitable trades. Stay well 🙏

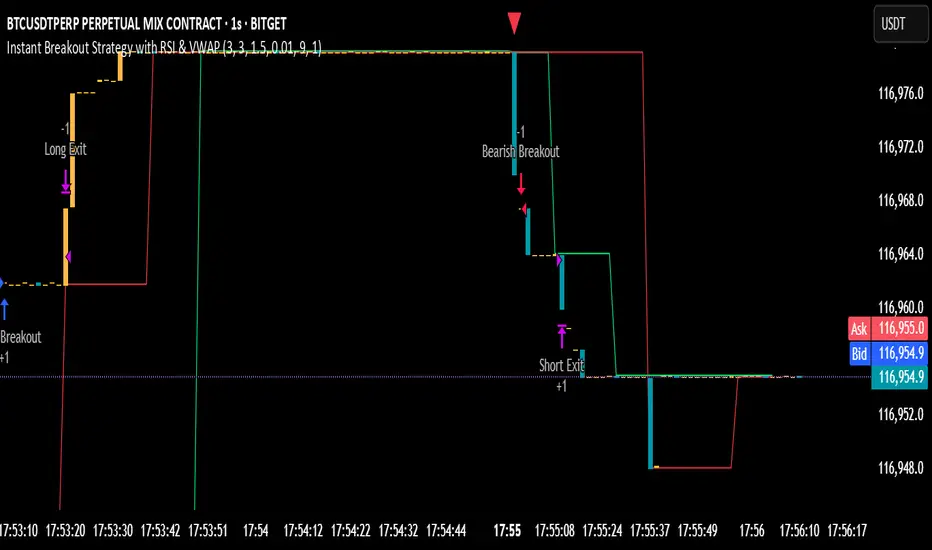

Instant Breakout Strategy with RSI & VWAPInstant Breakout Strategy with RSI & VWAP

This TradingView strategy (Pine Script v6) trades breakouts using pivot points, with optional filters for volume, momentum, RSI, and VWAP. It’s optimized for the 1-second timeframe.

Overview

The strategy identifies breakouts when price crosses above resistance (pivot highs) or below support (pivot lows). It can use basic pivot breakouts or add filters for stronger signals. Take-profit and stop-loss levels are set using ATR, and signals are shown on the chart.

Inputs

Left/Right Pivot Bars: Bars to detect pivots (default: 3). Lower values increase sensitivity.

Volume Surge Multiplier: Volume threshold vs. 20-period average (default: 1.5).

Momentum Threshold: Minimum % price change from bar open (default: 1%).

Take-Profit ATR Multiplier: ATR multiplier for take-profit (default: 9.0).

Stop-Loss ATR Multiplier: ATR multiplier for stop-loss (default: 1.0).

Use Filters: Enable/disable volume, momentum, RSI, and VWAP filters (default: off).

How It Works

1. Pivot Detection

Finds pivot highs (resistance) and lows (support) using ta.pivothigh and ta.pivotlow.

Tracks the latest pivot levels.

2. Volume Surge

Compares current volume to a 20-period volume average.

A surge occurs if volume exceeds the average times the multiplier.

3. Momentum

Measures price change from the bar’s open.

Bullish: Price rises >1% from open.

Bearish: Price falls >1% from open.

4. RSI and VWAP

RSI: 3-period RSI. Above 50 is bullish; below 50 is bearish.

VWAP: Price above VWAP is bullish; below is bearish.

5. ATR

14-period ATR sets take-profit (close ± atr * 9.0) and stop-loss (close ± atr * 1.0).

Trading Rules

Breakout Conditions

Bullish Breakout:

Price crosses above the latest pivot high.

With filters: Volume surge, bullish momentum, RSI > 50, price > VWAP.

Without filters: Only the crossover is needed.

Bearish Breakout:

Price crosses below the latest pivot low.

With filters: Volume surge, bearish momentum, RSI < 50, price < VWAP.

Without filters: Only the crossunder is needed.

Entries and Exits

Long: Enter on bullish breakout. Set take-profit and stop-loss. Close any short position.

Short: Enter on bearish breakout. Set take-profit and stop-loss. Close any long position.

Visuals

Signals: Green triangles (bullish) below bars, red triangles (bearish) above bars.

Pivot Levels: Green line (resistance), red line (support).

Indicators: RSI (blue, separate pane), VWAP (purple, on chart).

How to Use

Apply to a 1-second chart in TradingView for best results.

Adjust inputs (e.g., pivot bars, multipliers). Enable filters for stricter signals.

Watch for buy/sell triangles and monitor RSI/VWAP.

Use ATR-based take-profit/stop-loss for risk management.

Notes

Best on 1-second timeframe due to fast RSI and responsiveness.

Disable filters for more signals (less confirmation).

Backtest before live trading to check performance.

This strategy uses pivots, volume, momentum, RSI, and VWAP for clear breakout trades on the 1-second timeframe.

PowerTrend Pro Strategy – Gold OptimizedTired of false signals on Gold?

PowerTrend Pro combines VWAP, Supertrend, RSI, and smart MA filters with trailing stops & break-even logic to deliver high-probability trades on XAUUSD.

PowerTrend Pro Strategy is a professional-grade trading system designed to capture high-probability swing and intraday opportunities on XAUUSD (Gold) and other volatile markets.

🔑 Core Features

VWAP Anchoring – institutional fair value reference to filter trades.

Supertrend (ATR-based) – adaptive trend filter tuned for Gold’s volatility.

Multi-Timeframe RSI – confirms momentum alignment across intraday and higher timeframe.

EMA + SMA Combo – ensures trades follow strong directional bias, reducing false signals.

Dynamic Risk Management

Adjustable Take Profit / Stop Loss (%)

Trailing Stop that locks in profits on extended moves

Break-Even Logic (stop loss moves to entry once price is in profit)

⚡ Gold-Tuned Presets

XAUUSD 1H → tighter TP/SL & faster entries for active intraday trading.

XAUUSD 4H → wider ATR filter & trailing stops to capture bigger swings.

Generic Mode → works on Forex, Indices, and Crypto (fully customizable).

🎯 Why It Works

Gold is notoriously volatile — quick spikes wipe out weak strategies. PowerTrend Pro solves this by combining:

✅ Institutional bias (VWAP)

✅ Adaptive trend filter (Supertrend)

✅ Momentum confirmation (RSI MTF)

✅ Robust trend structure (EMA + SMA)

✅ Smart exits (TP, SL, trailing & breakeven)

This multi-layer confirmation makes entries stronger and keeps risk under control.

🛠️ Usage

Add the strategy to your chart.

Choose a preset (XAUUSD 1H, 4H, or Generic).

Run Strategy Tester for performance metrics.

Optimize TP/SL and ATR values for your broker & market conditions.

🔥 Pro Tip: Combine this strategy with a session filter (London/NY overlap) or volume confirmation to boost accuracy in Gold.

Valid H/L Strategy Tester with MFE/MAE Analytics

## Overview

A data-driven trading indicator that identifies valid high/low price levels and provides statistical insights through Maximum Favorable Excursion (MFE) and Maximum Adverse Excursion (MAE) analytics. Make informed trading decisions based on historical price behavior rather than guesswork.

## Key Features

### 🎯 Smart Pattern Recognition

- Automatically detects valid highs and lows with confirmation system

- Color-coded candles and lines for clear visual identification

- Inside/Outside print filtering for higher probability setups

### 📊 Statistical Analytics

- Analyzes up to 500 historical setups for MFE/MAE calculations

- 1-hour and 3-hour timeframe data with percentile-based targets (20th, 50th, 80th)

- Real-time performance tracking with comprehensive statistics table

### ⚙️ Flexible Strategy Options

**Entry Methods:** Confirmation-based or MAE percentile entries

**Take Profit:** MFE-based, fixed points, percentage, or R:R ratio targets

**Risk Management:** Multiple stop loss types with position sizing controls

### 🕐 Advanced Time Filtering

- Session filters (Asia, London, New York)

- Individual hourly controls (24-hour precision in ET)

- Pre-configured for optimal NY trading hours (9 AM - 2 PM)

### 📈 Visual Dashboard

- MFE target lines (blue) and MAE risk lines (orange)

- Customizable colors, styles, and line weights

- Statistics table showing daily/hourly/weekly performance breakdowns

## How It Works

1. **Pattern Detection** - Scans for valid high/low formations using price structure and gap behavior

2. **Statistical Analysis** - Calculates historical MFE/MAE percentiles from past setups

3. **Trade Framework** - Executes entries/exits based on your configuration with real-time performance tracking

## Ideal For

- **Day/Swing Traders** seeking data-driven entry/exit levels

- **Risk Managers** wanting historical drawdown data for stop placement

- **Performance Trackers** needing detailed analytics across timeframes and sessions

- **Flexible Strategies** - adapts to scalping, day trading, or swing trading styles

## Quick Setup

1. Select analysis timeframe (default: 5-minute)

2. Choose entry method and exit strategy

3. Enable MFE/MAE analytics display

4. Apply session/hourly filters

5. Customize visual elements and table settings

Transform your trading from guesswork to statistical precision with historical price behavior insights.

Three-Step 9:30 Range Scalping# Three-Step 9:30 Range Scalping Strategy Rules

## Step 1: Mark the Levels (9:30 AM)

- Wait for the **first 5-minute candle** starting at 9:30 AM EST to close

- Mark the **HIGH** and **LOW** of this candle

- Switch to **1-minute chart** for trading

## Step 2: Find Your Entry (Trade for 1 hour only: 9:30-10:30 AM)

### BREAK Entry

- Need: **Fair Value Gap (FVG)** + **ANY** of the 3 FVG candles closes outside the range

- FVG = Gap between candle wicks (3-candle pattern)

### TRAP Entry

- Need: Break outside range → Retest back inside → Close back outside again

### REVERSAL Entry

- Need: Failed break in one direction → Opposite FVG back into the range

## Step 3: Trade Management

### Stop Loss:

- **Break/Trap**: Low/High of first candle that closed outside the range

- **Reversal**: Low/High of first candle in the FVG pattern

### Take Profit:

- **Always 2:1 risk-to-reward ratio**

- If you risk $100, you make $200

## Key Rules:

- ✅ **Body close** outside range (not just wicks)

- ✅ Trade on **1-minute chart** only

- ✅ Only trade **first hour** (9:30-10:30 AM EST)

- ✅ **Fixed 2:1** take profit every time

- ✅ One strategy, stay consistent

**That's it. No complicated indicators, no higher timeframe bias, no guesswork.**

Supertrend Strategy with ATR TP and SLSupertrend Strategy with ATR TP and SL

Overview

The Supertrend strategy is a trend-following trading system that utilizes the Average True Range (ATR) to determine the market's volatility and to set dynamic support and resistance levels. This strategy employs the Supertrend indicator to identify entry and exit points for trades, specifically focusing on long and short positions in the market.

Key Components

Inputs

ATR Period: This defines the lookback period for calculating the ATR, which helps in understanding market volatility. The default value is set to 10.

Supertrend Multiplier: This multiplier adjusts the sensitivity of the Supertrend indicator. A value of 3 is used, affecting the upper and lower bands of the Supertrend calculation.

TP (Take Profit) ATR Multiplier: This multiplier is used to calculate the take profit level based on the ATR (default value is 3).

SL (Stop Loss) ATR Multiplier: This multiplier dictates the stop loss distance from the entry point concerning the ATR, set to a value of 1.5.

Number of Bars to Use for Backtest: This setting determines how many bars are analyzed during testing, set to a default of 240.

Trading Mode: Options are provided to choose whether to take only long positions or only short positions.

ATR Calculation

The ATR is computed using a specified period, allowing traders to gauge market volatility effectively. This is crucial for setting appropriate stop loss and take profit levels.

Supertrend Calculation

The Supertrend indicator is calculated using the ATR and the multiplier to derive upper and lower bands. The current market price is compared against these bands to determine the trend direction.

Trade Signals

Buy Signal: Generated when the price closes above the Supertrend line, indicating a potential upward trend.

Sell Signal: Generated when the price closes below the Supertrend line, indicating a potential downward trend.

Entry and Exit Strategies

When a buy signal is triggered, the strategy will enter a long position while setting the take profit and stop loss based on the ATR values.

Conversely, if a sell signal occurs, a short position is opened with respective take profit and stop loss levels.

Alert Conditions

Alerts are set up for both buy and sell signals, allowing users to be notified when trade opportunities arise.

Visualization

The Supertrend line is plotted on the chart, along with take profit and stop loss levels for each trade. Labels indicate entry points to facilitate easy tracking of trades.

Conclusion

This Supertrend strategy is designed to simplify trading decisions by automating the entry and exit points based on well-defined market conditions. By utilizing the ATR for dynamic risk management, traders can adapt their approach according to market volatility. This strategy is suitable for many trading styles and can be backtested to assess its performance across different market conditions.

Usage

To use this strategy, simply apply the script in TradingView and adjust the input parameters based on your trading preferences. The strategy can be modified further to enhance its performance according to specific market scenarios.

Valdes Trading Bots - Scaled Profits and DCA — V 12.1Valdes Trading Bots – Scaled Profits and DCA — V 12.1

Overview

This strategy is built for traders who want to capture medium-term swings without getting caught in short-term noise. It is optimized for the 12-hour timeframe, where signals have historically shown stronger consistency across a wide range of market conditions.

Key Features

Trend regime detection – Identifies when momentum flips from bullish to bearish (and vice versa).

Scaled profit targets – Positions automatically reduce across multiple take-profit levels to secure gains progressively.

Risk management – Includes a capped, rules-based averaging (DCA) method during controlled pullbacks. Not martingale, strictly limited.

Directional flexibility – Can operate long or short, depending on market regime.

JSON output included – Adds flexibility for advanced users.

How to Use

Apply primarily on the 12-hour chart for best results.

Use this script for backtesting, research, and simulation before any live application.

No input changes are required; it is designed to run as-is.

Notes & Limitations

This is a strategy script, not a signal service.

Past win rates or backtest results are not predictive of future performance.

All markets carry risk, and losing trades will occur.

Always test extensively in paper trading before deploying to a live account.

Disclaimer

This script is provided for educational and research purposes only. It is not financial advice. The authors and publishers assume no responsibility for losses incurred from using this strategy.

No Wick Strategy (No-wick candles) — by Sh1n1gam1**No Wick Strategy - Momentum Trading System**

This strategy identifies and trades "no wick" or "minimal wick" candles, which often indicate strong directional momentum and conviction in the market.

**STRATEGY CONCEPT:**

The No Wick Strategy capitalizes on candles that show strong directional commitment - bullish candles with little to no bottom wick (buyers in control from the start) and bearish candles with little to no top wick (sellers dominating from the open).

**HOW IT WORKS:**

📈 **LONG ENTRIES:**

- Identifies bullish candles with minimal/no bottom wick

- Places buy limit order slightly below the signal candle's open

- Enters only during specified trading session

📉 **SHORT ENTRIES:**

- Identifies bearish candles with minimal/no top wick

- Places sell limit order slightly above the signal candle's close

- Enters only during specified trading session

**KEY FEATURES:**

✅ Customizable trading session (New York timezone)

✅ Flexible wick threshold (0% for strict, up to X% for flexibility)

✅ ATR-based stop loss for dynamic risk management

✅ Configurable risk-reward ratio via TP multiplier

✅ Auto-cancellation of unfilled orders after X bars

✅ Body size filters (minimum and maximum)

✅ Visual signals and pending order levels

✅ Position status display

**RISK MANAGEMENT:**

- Stop Loss: Based on ATR multiplier

- Take Profit: Multiple of stop loss distance

- One position at a time

- No pyramiding or position flipping

**RECOMMENDED TIMEFRAMES:**

- M1 and M5 for scalping

- M15 and H1 for day trading

- H4 and Daily for swing trading

**MARKETS:**

Suitable for forex pairs, indices (NQ, ES), commodities, and liquid stocks.

**DEFAULT SETTINGS:**

- Trading Session: 09:30-11:00 ET (NY morning session)

- ATR SL Multiplier: 1.5

- TP Multiplier: 2.0 (2:1 RR ratio)

- Wick Threshold: 5%

- Order Cancellation: 5 bars

**TIPS FOR OPTIMIZATION:**

1. Adjust trading session to match your market's most active hours

2. Test different wick thresholds (0-10%) based on market volatility

3. Optimize body size filters for your specific instrument

4. Backtest different ATR multipliers for your risk tolerance

5. Consider market conditions - works best in trending markets

**IMPORTANT NOTES:**

- Uses limit orders for better entry prices

- Does not close opposing positions (no position flipping)

- Respects trading session boundaries strictly

- All times are in America/New_York timezone

**AUTHOR:** Sh1n1gam1

**VERSION:** 1.0

**SUPPORT:** Comments and suggestions welcome!

Happy Trading! 📊

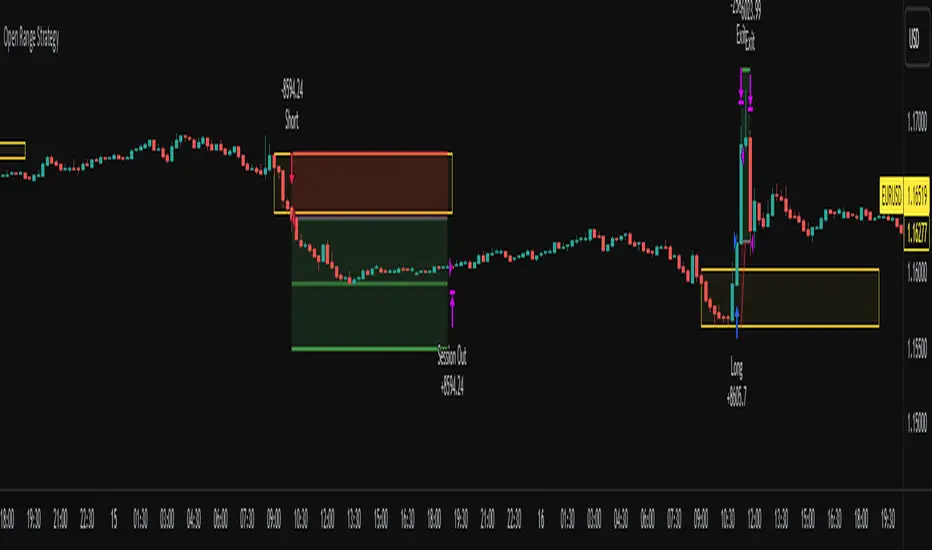

Open Range Breakout Strategy With Multi TakeProfitHello everyone,

For a while, I’ve been wanting to develop new scripts, but I couldn’t decide what to create. Eventually, I came up with the idea of coding traditional and well-known trading strategies—while adding modern features such as multi–take profit options. For the first strategy in this series, I chose the Open Range Strategy .

For those unfamiliar with it, the Open Range Strategy is a trading approach where you define a specific time period at the beginning of a trading session—such as the first 15 minutes, 30 minutes, or 1 hour—and mark the highest and lowest prices within that range. These levels then act as reference points for potential breakouts: if the price breaks above the range, it may signal a long entry; if it breaks below, it may indicate a short entry. This method is popular among day traders for capturing early momentum in the market.

Since this strategy is generally used as an intraday strategy , I added a Trade Session feature. This allows you to define the exact time window during which trades can be opened. Once the session ends, all positions are automatically closed, ensuring trades remain within your chosen intraday period.

Even though it’s a relatively simple concept, I’ve come across many different variations of it. That’s why I created a highly customizable project. Under the Session Settings, you can select the time window you want to define as your range. Whether it’s the first 15-minute candle or the entire first hour, the choice is entirely yours.

For stop-loss placement, there are two different options:

Middle of the Range – The stop loss is placed at the midpoint between the high and low of the defined range, offering a balanced buffer for both bullish and bearish setups.

Top/Bottom of the Range – The stop loss is placed just beyond the range’s high for short trades or just below the range’s low for long trades, providing a more conservative risk approach.

I’ve always been a big fan of the multi take-profit feature, so I added two different take-profit targets to this project. Take profits are calculated based on a Risk-to-Reward Ratio, which you can adjust in the settings. You can also set different position sizes for each target, allowing you to scale out of trades in a way that suits your strategy.

The result is a flexible, user-friendly strategy script that brings together a classic approach with modern risk management tools—ready to be tailored to your trading style

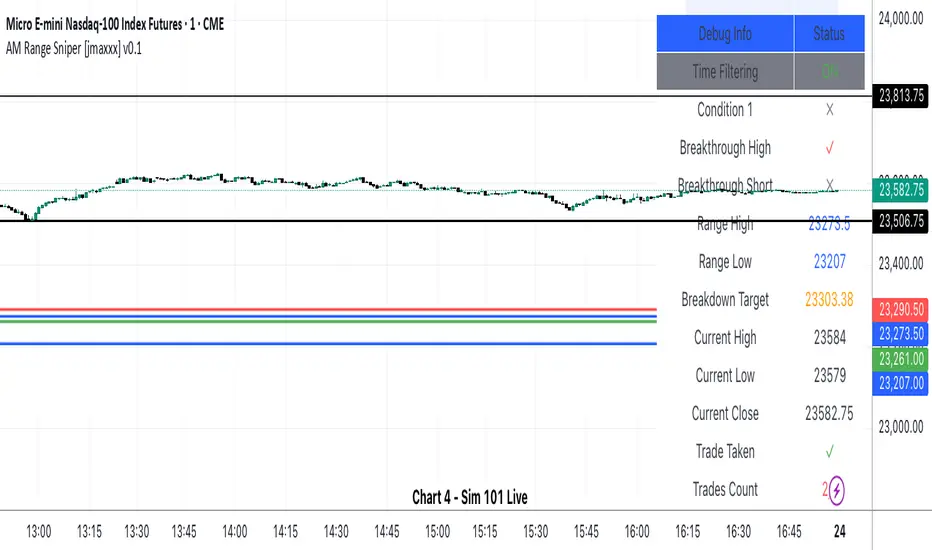

AM Range Sniper [jmaxxx]AM Range Sniper

Overview

AM Range Sniper is a sophisticated morning session trading strategy designed for Micro E-mini Nasdaq-100 Index Futures (MNQ). This strategy capitalizes on the critical 8:30-9:30 AM EST range formation period, implementing precise entry and exit mechanics with advanced risk management.

Key Features

🕐 Time-Based Range Analysis

Range Definition: Automatically identifies and tracks the 8:30-9:30 AM EST range

Trading Window: Active trading from 9:30 AM to 11:00 AM EST (extended for second chance trades)

Session Management: Daily reset ensures clean state for each trading session

🎯 Multiple Entry Patterns

Breakthrough/Retest: Captures price breakthroughs above range with retest opportunities

Long/Short Opportunities: Comprehensive coverage of both directional moves

Breakdown: Identifies bearish breakdowns below range support

Break Up: Detects bullish breakups above range resistance

Range Sweeps: Monitors for range high/low sweeps with reversal entries

⚡ Advanced Risk Management

Configurable Stop Losses: Tick-based stop losses for each trade type

Take Profit Targets: Automatic target calculations based on range size

Hard Close Protection: Automatic position closure at 4 PM EST

Second Chance Feature: Optional second trade opportunity if first trade loses

🔧 Professional Features

Visual Stop Loss Lines: Real-time stop loss visualization on chart

Debug Information Panel: Comprehensive status monitoring

Alert Integration: Customizable alert messages for entries/exits

Flexible Time Settings: Adjustable for different timezones

Strategy Logic

Range Formation (8:30-9:30 AM)

The strategy monitors the first hour of trading to establish the day's range. This range serves as the foundation for all subsequent trading decisions.

Entry Conditions

Breakthrough: Price breaks above range high with retest rejection

Breakdown: Price breaks below range low with confirmed bearish momentum

Break Up: Price breaks above range high with strong bullish confirmation

Sweep Entries: Range high/low sweeps followed by reversal signals

Risk Management

Stop Loss: Configurable tick-based stops for each trade type

Take Profit: 1.5x range size targets for breakdown/breakup trades

Position Sizing: Percentage-based position sizing

Session Limits: Maximum 2 trades per session (with second chance feature)

Settings & Customization

Core Parameters

Enable/disable individual entry patterns

Configurable stop loss levels (1-500 ticks)

Second chance feature toggle

Previous day level integration

Visual Customization

Customizable stop loss colors and widths

Debug panel visibility

Range line styling

Alert Configuration

Custom entry/exit alert messages

***** Automate With *****

APEX

NinjaTrader

Crosstrade.io ( promo code JMAXXX )

Performance & Reliability

Precision Focused: Waits for high-probability setups

Risk-Aware: Comprehensive stop loss and position management

Session-Based: Clean daily resets prevent carryover issues

Professional Grade: Designed for serious traders

Ideal For

Day Traders: Morning session specialists

Futures Traders: MNQ and similar instruments

Range Traders: Traders who capitalize on range breakouts

Risk-Conscious Traders: Those who prioritize risk management

Disclaimer

This strategy is for educational and informational purposes. Past performance does not guarantee future results. Always test thoroughly on historical data and paper trading before live implementation. Risk management is crucial - never risk more than you can afford to lose.

Created by jmaxxx - Professional trading strategy developer

For questions, feedback, or customization requests, please leave a comment below.

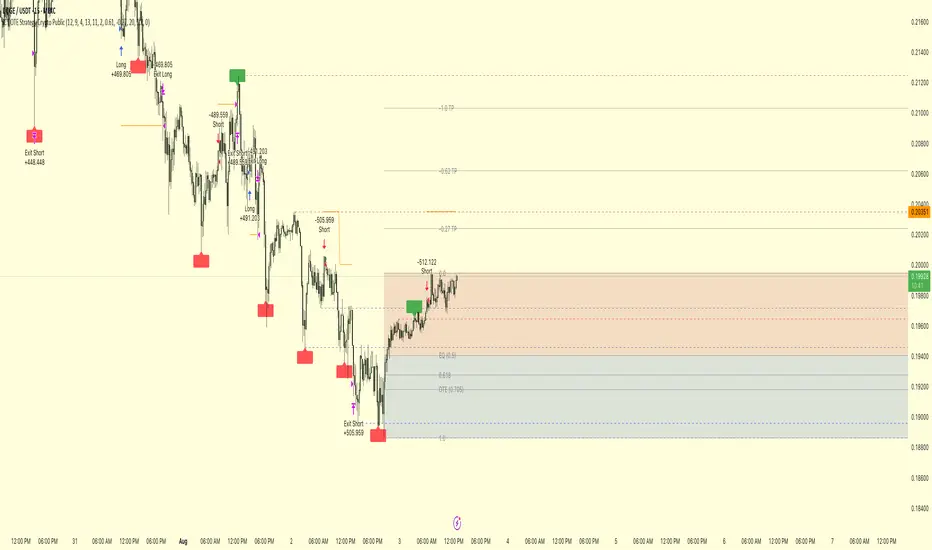

ICT OTE Strategy Crypto PublicICT OTE Strategy Crypto Public

This strategy automates a classic ICT (Inner Circle Trader) setup specifically tailored for the high-volatility nature of cryptocurrency markets. It aims to enter a trade on a retracement after a confirmed Break of Structure (BOS), using a dual-swing detection method to validate the market's direction before looking for an entry.

The entire process is automated, from identifying the market structure to managing the trade with advanced risk management options. This version uses a percentage of equity for its order sizing, which is ideal for crypto trading.

How It Works

Dual Swing Detection: The strategy uses two different sets of swing strengths to analyze market structure for higher accuracy:

Entry Swings: Weaker, more sensitive swings used to define the immediate dealing range for a potential trade.

Validator Swings: Stronger, more significant swings used to confirm a true Break of Structure.

Break of Structure (BOS): A trade setup is only considered valid after a strong "Validator" swing breaks through a previous "Entry" swing. This confirms the market's intended direction and filters out weak or false moves.

Identify Retracement Leg: After a confirmed BOS, the strategy identifies the most recent "Entry Swing" price leg that led to the break.

Auto-Fibonacci: It automatically draws a Fibonacci retracement over this leg, from the start of the move (1.0) to the end (0.0).

Trade Entry: A limit order is placed at a user-defined Fibonacci level (defaulting to 0.618), anticipating a price pullback into a discount or premium array.

After a bullish BOS, it looks to BUY the retracement.

After a bearish BOS, it looks to SELL the retracement.

Risk Management:

Stop Loss is placed at the start of the leg (the 1.0 level).

Take Profit is placed at a user-defined level (defaulting to the 0.0 level, with extension options).

Includes an option to move the stop loss to break-even after the trade has moved a certain distance in profit.

How to Use

Asset Selection: This strategy is designed for cryptocurrency markets. Its use of percentage-based order sizing is not suitable for tick-based markets like futures.

Swing Settings: Adjust the "Entry Swing" and "Validator" strengths to match the volatility and timeframe of the asset you are trading. Higher numbers will result in fewer, more significant setups.

Backtest: Use the Strategy Tester to optimize the "FIB Entry Level," "Take Profit Level," and "Swing Sensitivity" to find the best settings for your specific market and timeframe.

ICT OTE Strategy Futures PublicICT OTE Strategy

This strategy automates a classic ICT (Inner Circle Trader) setup that aims to enter a trade on a retracement after a confirmed Break of Structure (BOS). It is designed to identify high-probability setups by waiting for the market to show its hand before looking for an entry within a "discount" or "premium" array.

The entire process is automated, from identifying the market structure to managing the trade with a dynamic stop loss.

How It Works

Break of Structure (BOS): The strategy first waits for a strong, validated swing to break a previous, weaker swing high or low. This confirms the market's intended direction.

Identify Retracement Leg: After a BOS, the strategy identifies the most recent price leg that led to the break.

Auto-Fibonacci: It automatically draws a Fibonacci retracement over this leg, from the start of the move (1.0) to the end (0.0).

Trade Entry: A limit order is placed at a user-defined Fibonacci level (defaulting to 0.508), anticipating a price pullback.

After a bullish BOS, it looks to BUY the retracement.

After a bearish BOS, it looks to SELL the retracement.

Risk Management:

Stop Loss is placed at the start of the leg (the 1.0 level).

Take Profit is placed at a user-defined level (defaulting to the 0.0 level).

Includes an option to move the stop loss to break-even after the trade has moved a certain distance in profit.

How to Use

Swing Settings: Adjust the "Entry Swing" and "Validator" strengths to match the volatility and timeframe of the asset you are trading. Higher numbers will result in fewer, more significant setups.

Session Filter: Use the "Trading Sessions" filter to align the strategy with ICT's "killzone" concept, ensuring trades are only taken during high-volume periods like the New York session.

Backtest: Use the Strategy Tester to optimize the "FIB Entry Level," "Take Profit Level," and "Min Trade Range" to find the best settings for your specific market and timeframe.